How to Think Like an Investor: Understanding the Actual Cost of Fundraising

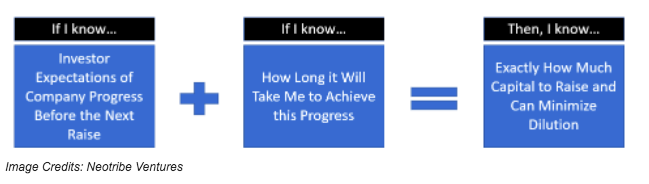

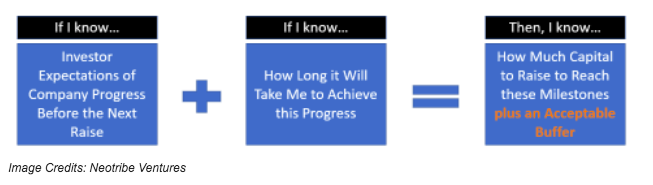

Investors want you to raise enough capital to comfortably reach your financial and non-financial targets before another fundraise — raise what you expect to need plus an acceptable buffer.

Why is venture funding so confusing? Isn’t the formula simple?

Well, to start, the presumption that a company knows what its investors expect with full clarity is a lofty one. Investors will have both financial and non-financial milestones they expect a company to achieve between raises, and these milestones can differ greatly between stages.

Even with this information, it can be difficult to project how long it will take to achieve these goals. Finally, is it even correct to assume that minimizing dilution is the singular goal?

With the caveat that every company journey, fundraising environment and investor preference is different, let’s put aside all of the truths we think we know and start at the beginning.

In all likelihood, the first question a founder must answer is how much money to raise. This question considers a lot of inputs, but the three that are the most opaque to founders are:

- How expensive is venture capital (as defined by the amount of dilution)?

- What financial milestones will investors expect me to reach between each raise?

- What are the more subjective milestones I need to hit to evidence I’m ready for the next raise?

Let’s take these questions one at a time.

How expensive is venture capital?

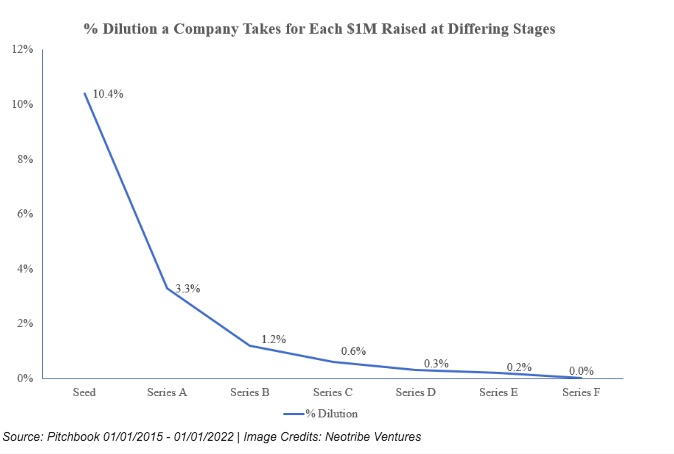

Before we address the inputs in the equation, we need to understand if the output — minimizing dilution — is exactly what we should solve for during each raise. To do this, let’s look at the median amount of dilution companies have taken at each stage over the last several years. To put it into useful context, let’s look at dilution for each $1 million raised.

This graph shows us that for every $1 million raised in a seed round, it costs ~10% of the company. By Series B, the dilution per $1 million falls to ~1.2%, and by Series E, each $1 million of capital raised costs ~0.2%.

In other words, the cost of capital dramatically decreases as a company grows. This deep decline in the cost of funding at progressive fundraises is what I like to call the Venture Capital Price Curve.

Does the Venture Capital Price Curve prove that the singular goal of a company fundraise should be to minimize dilution? Not quite.

For later-stage raises (e.g., Series D and beyond), capital is relatively inexpensive. During this phase, companies will often “build a war chest” to tackle market opportunities because the incremental dilution incurred is relatively small. The math is different in the early stages when the cost of capital, and thus dilution, impact is higher. For these stages, the data tells us that dilution should be a strong consideration in how much to raise — but, should it be the only consideration?

The answer is still no. Capital is dramatically more expensive at the early stages because there are major risks involved and the probability of a successful outcome is low. Because the risk of failure is highest at the seed stage, the cost of capital is also the highest.

In order to get to the next phase of capital raising, founders must raise enough capital to de-risk the company. It is not prudent to try to raise the “optimal” amount to minimize dilution because of the substantial risk that they cut too closely and are unable to meet milestones and raise more capital.

Knowing the cost of capital should dissuade you from significantly over-raising in the early stages, but it should not dissuade you from raising the required amount of capital to get the company to the next stage — with a little breathing room.

With this information, we have a new equation.

We’ve introduced a new term: “acceptable buffer.” Given our prior discussion, we should define the acceptable buffer differently at each stage. For example, a $30 million buffer may be acceptable at the Series D given the cost of capital, while a $1 million buffer may be preferred at the seed stage.

Of course, a company will solve for factors other than dilution (e.g., resources of the investing partner/firm, their expertise in the field, their ability to contribute future capital, etc.). This framework isn’t meant to inform which investor you should choose, but rather it informs how you should think about how much capital you should go out to raise.

There is no substitute for a partner who can source key hires, advise on finding product-market fit and help you avoid pitfalls along the way. That said, it will benefit you to be knowledgeable about the size of the raise you are targeting during investor conversations.

Now that we understand the cost of venture funding, we need to address which milestones investors will expect to see in between each raise to help us determine how much to raise.

Financial milestones to be met between raises

Revenue and revenue growth are two of the most ubiquitous financial metrics investors will evaluate at every stage. While these metrics are clearly important, investor expectations of these metrics at each stage can vary dramatically depending on the market environment.

To be more specific, in bear markets, a company may need revenue of more than $15 million to attract Series B investors. In a bull market, the same company may only need revenue of $5 million to attract investors. Since you cannot control the market environment you are raising in, it is good to understand what the long-term trends are in terms of investor revenue expectations.

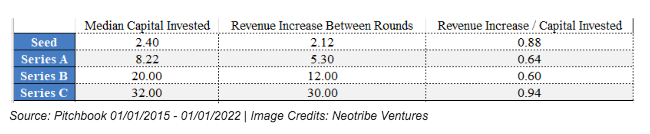

For the sake of providing broader guidance versus environment-specific guidance, let’s use the same dataset that generated the Venture Capital Price Curve to help us determine how much to raise. We can use it to see the median ratio of capital raised to revenue growth between each round of funding.

This ratio will allow us to understand the broad expectations for required growth in between rounds. For our purposes, we are showing the changes from seed to Series A to B to C. Capital invested and revenue numbers are in millions of USD.

Median ratio of capital raised to revenue growth between each round of funding.

While this chart tells us a number of things, let’s focus on the key points. As an example, the median seed round raised in this time was $2.4 million. These companies were able to increase revenue between their seed and Series A rounds by $2.12 million.

This creates a ratio of revenue increase ($2.12 million) divided by capital invested ($2.4 million) of 0.88. Similarly, the median capital invested for Series A companies was $8.2 million, and so on.

This chart confirms our intuition that companies raise larger rounds as they progress, as well as that the quantum of revenue increases continue to grow as companies scale.

This also tells us that the efficiency of each dollar to revenue generation is highest at the seed and Series C stages. Why?

Generally, a company can generate some revenue from early adopters or revenue generating proof-of-concepts (PoCs). This small amount of revenue can often be generated with a small amount of capital. When a company moves to Series A and Series B, while technology and product are de-risked, figuring out the go-to-market motion requires investment.

A company must invest in sales and marketing and likely try a number of different strategies before it can determine the most efficient path ahead. In these years, the ratio decreases to about 60%. By Series C, the company is more efficiently putting investments behind strategies it knows will generate a return, and so, the ratio increases to 90%.

Broadly speaking, recent history tells us that investors require an increase in revenue that is roughly at least 60% or more of what you raise. While that may seem off-market in today’s environment, this is reflective of the median over the past seven years. A startup’s private journey can often be lengthy and span multiple market environments. Keep this in mind when thinking about future investor expectations.

Let’s look at an example. You want to raise a Series B, but don’t know how much to raise. Based on conversations with existing investors, you believe raising capital approximately every 24 months would be ideal. Based on your projections, you will increase revenue by $15 million over the next two years.

Our table would suggest that you can comfortably raise about $25 million for your Series B (i.e., $15 million/0.6), and that the $15 million increase in revenue will meet investor expectations. However, the market environment is telling you that you can raise $40 million.

If you elect to raise $40 million and the market environment changes back to the median reflected in the last seven years, generating an additional $15 million off a $40 million raise will be below the median of your peers (0.375 revenue increase to capital raised ratio).

Subjective milestones to meet to prove you’re ready for the next round

I’ll again put forward the caveat that all situations and investors are unique, but there are some common examples of progress that investors look for at each stage.

Stage: Seed | Investor priority: De-risk

It is all about de-risking existential threats at the seed stage. Investors are pricing in significant risk of failure of the technology, execution and/or the market. Founders must try to use their capital to prove that they have de-risked the critical areas before the Series A.

How do you prove that you have de-risked the company? While early revenue is a plus here, expectations are muted (as shown earlier). More relevant examples of de-risking include first customer deployments of the technology, hiring of key talent required to get the product to market and development of patents/proprietary data.

Stage: Series A | Investor priority: Develop

With technology and market risk hopefully addressed, what’s the main goal during the Series A? This stage is about developing the go-to-market strategy and a product roadmap.

As shown previously, the cost of a Series A is about a third of that of the seed. This allows companies to raise more capital for less dilution and use this capital to test various go-to-market motions, begin thinking about product or geographic expansion and expand the team to support these new initiatives.

Revenue generation in this phase becomes more critical in determining success, as it provides evidence of customer interest and willingness to pay, though it is likely still very difficult to predict.

Stage: Series B | Investor priority: Double down

Metrics, metrics, metrics. By the time you raise your Series B, investors likely have plenty of data to sift through and will look at key metrics like revenue growth, gross margin and customer expansion. Know the core metrics for your industry and what investors may be using as benchmarks.

At this stage, investors will expect you to have a management team, an identified go-to-market motion, a very clear idea of your ideal customer and the ability to forecast your financials with some predictability.

With all of this data, investors want you to double down on what is working, particularly sales and marketing efforts.

Stage: Series C and beyond | Investor priority: Domination

Investors at the Series C stage and beyond are likely looking for domination. At these stages, they look for category leaders that are consistently beating the competition and hitting financial targets. This often correlates to a low cost of capital, as investors are backing something that is already working well.

Parting thoughts

At the end of the day, investors want you to raise enough capital to comfortably reach your financial and non-financial targets before another fundraise — raise what you expect to need plus an acceptable buffer. Doing so alleviates stress on the founders, employees and, of course, the investors.

Understanding the expectations of the milestones achieved is an ongoing process as the company grows and the market environment changes, but it is important to stay current while also having a broader historical perspective.